Grantor Annuity Trusts (GRATs) and Intentionally Defective Grantor Trusts (IDGTs) vehicles offer the advantage of effectively ‘freezing’ asset values, thereby sheltering future appreciation from estate taxes, however they come with some key drawbacks:

Loss of step-up in basis – assets held forfeit the benefit of a step-up in basis upon the grantor’s death, potentially subjecting them to income taxes upon sale.

Tax Liability – grantors are obligated to cover taxes on trust assets, irrespective of whether they have the necessary income.

Annuity Payment Constraints – making payments may necessitate selling assets within the trust, diminishing potential.

Estate Inclusion – if grantor passes away during the trust’s term, all remaining assets become a part of the estate.

Narrower spread in high-Interest rate environments – narrower spread between earned rates and owed interest rates on borrow diminishing advantages.

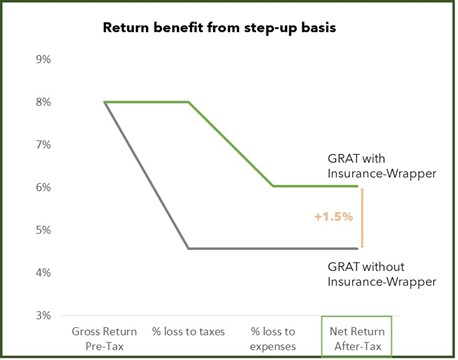

Insurance structures can usually be combined with GRATs to fill gaps and enhance investment returns if structured properly.